General overview CBAM

Why is the EU launching the CBAM?

Climate change is a big problem that needs solutions from all over the world. The European Union (EU) is trying to do more to help the climate, but other countries may not be as strict. This can lead to 'carbon leakage', where EU companies move their work to places with easier rules, or where EU products are replaced by imports that cause more pollution.

When will it start?

The CBAM will start a test phase on 1 October 2023, and companies will have to report for the first time by 31 January 2024. This slow start will allow businesses and governments in the EU and other countries to adapt in a controlled way. Initially, companies will only have to report the pollution in their imports, without having to pay for it. From 2026, companies will have to say how much they import each year and how much pollution is in those goods. They will have to buy CBAM certificates, the cost of which will depend on EU ETS prices. The EU will stop giving out free pollution permits while CBAM starts, from 2026 to 2034.

Who will be affected?

The scope of the Carbon Border Adjustment Mechanism (CBAM) is initially targeted at specific imports known for their substantial carbon footprints. Industries producingcement, iron, steel, aluminum, fertilizers, electricity, and hydrogen will be the first to feel the impact of CBAM. These sectors have been identified due to their significant contributions to pollution, and there's a recognized risk of these industries relocating outside the EU to regions with less stringent environmental regulations. CBAM is expected to encompass over half of the carbon impact within the European Union's Emissions Trading System (ETS). This gradual expansion underscores CBAM's commitment to comprehensive carbon pricing across diverse industries.

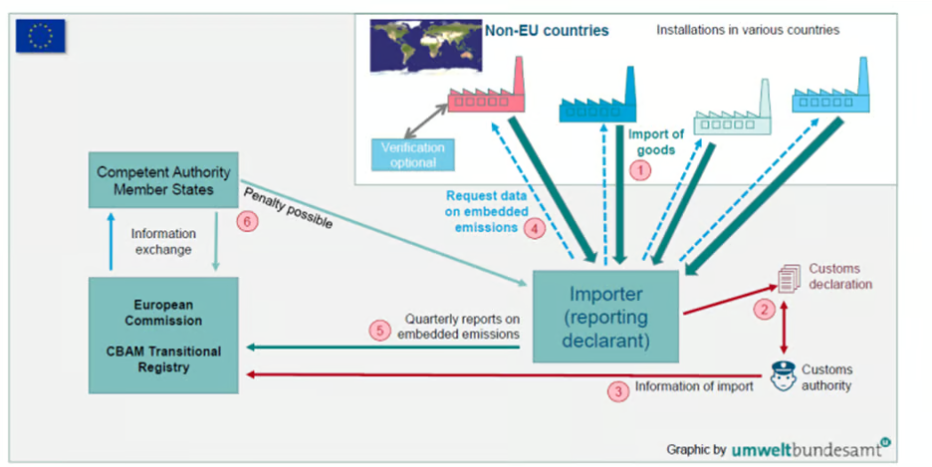

Whitin CBAM, the central responsibility lies with the importer. However, several other stakeholders are also involved (see figure below):

- Importers: Importers are businesses or entities within the European Union that bring in goods from outside the EU. Under CBAM, importers are obligated to purchase and prove carbon certificates corresponding to the embedded carbon costs of the imported products.

- Exporters: These are businesses or entities responsible for producing and exporting goods to the European Union. Exporters should report relevant information about the emissions associated with the production of their goods to importers.

- Authorities: Both at European level and Member State level, governmental bodies are responsible for implementing and overseeing CBAM (National customs, European Commission, Competent National Authority). These authorities are tasked with verifying the accuracy of the information provided by exporters and importers, ensuring compliance with CBAM regulations, and managing the issuance and redemption of carbon certificates.

Any sanctions to be afraid of?

During the transitional period, sanctions are raised for absence, incorrect or incomplete reports. These sanctions can mount to between 10 to 50 euros per ton CO2 that not correctly reported.

During the definitive period the sanctions are raised for importations of CBAM goods without any authorizations. These sanctions can mount to between 300 to 500 euros per ton CO2 without any authorizations.

What should be reported?

Under CBAM, reporting requirements for importers are focused on the carbon content of certain imported goods. The primary goal is to account for the emissions associated with the production of these goods, ensuring that carbon costs are reflected in their pricing as they enter the European Union market. Here are the key aspects that need to be reported under CBAM:

- Quantity of Imported Goods Covered: Importers are required to report the quantity of imported goods covered by CBAM.

- Emission Data for Imported Goods: Importers must now report how much greenhouse gases are made when producing goods they bring into the country. In the transition phase, the importers needs to include both direct and indirect emissions. In the definitive phase, they will only report direct emissions. The boundaries of the embedded emissions matches the EU's carbon trading system, not the full life cycle emissions as in the GHG Protocol (e.g. Scope 3.1 Goods & Services). Importers should try to get exact emissions data from their suppliers. Until July 2024, they can estimate using default values as much as they need. After that, they can only estimate up to 20% of the emissions with these values.

- Carbon pricing: If the exporting country has carbon pricing mechanisms in place, these are taken into account. Importers can report the cost already incurred for carbon pricing in the country of origin, which can be offset against the CBAM costs.

- Verification and Documentation: Importers are required to provide verified documentation of the carbon emissions associated with their imported products. This may involve third-party verification to ensure accuracy and compliance with the EU's standards.

- Carbon Pricing Compliance: Importers must purchase and surrender CBAM certificates, which represent the carbon price that would have been paid if the goods were produced under the EU's carbon pricing policies. The number of certificates correlates with the tonnage of carbon dioxide emissions embedded in the imported products.

Note that reporting aspects 4-5 are only required as of the definitive phase from January 2026 onwards, while reporting aspects 1-3 are already required as of the transition phase from October 2023.